Your CIBIL score is one of the most important thing that show your financial health. Whether you want a personal loan, home loan, car loan, or even a credit card, lenders check your credit score before approving your application. A higher score not only improves your chances of approval but also helps you get loans at lower interest rates.

If your credit score is low, don’t worry. With the right steps and discipline, you can improve your CIBIL score over time. In this article, we will explain what a CIBIL score is, why it matters, and the best ways to increase it.

What is a CIBIL Score?

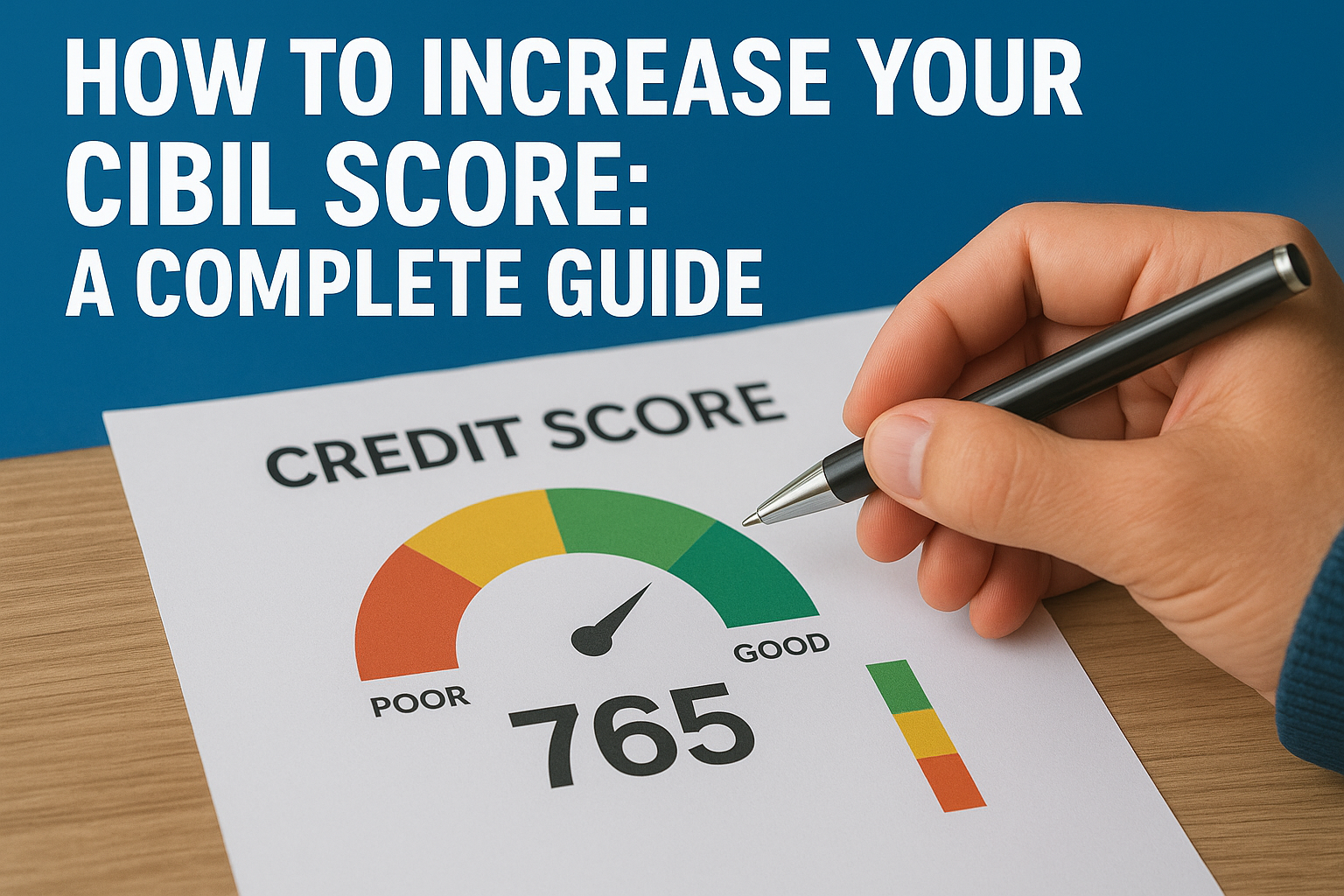

A CIBIL score, also known as a credit score, is a 3-digit number ranging between 300 and 900. It is issued by TransUnion CIBIL, one of India’s leading credit info company.

- 300–549 → Poor (High risk of default)

- 550–649 → Average (Needs improvement)

- 650–749 → Good (Eligible for loans, but not best offers)

- 750–900 → Excellent (Easily eligible for loans with low interest rates)

- The higher your score, the better your creditworthiness in the eyes of banks and financial institutions.

Why is CIBIL Score Important?

- Loan Approval – Banks and NBFCs prefer lending to people with a good credit score.

- Higher Credit Limit – Credit cards with high limits are usually offered to people with strong scores.

- Faster Processing – A good score speeds up approval for loans and credit cards.

- How to Increase Your CIBIL Score

If you want to improve your CIBIL score, follow these practical steps:

Pay Your Bills and EMIs on Time

- Timely payment of credit card bills and loan EMIs has the biggest impact on your credit score. Even a single missed or delayed payment can reduce your score significantly. Always:

- Set reminders or auto-debit options for payments.

- Clear at least the minimum due amount on credit cards, though full payment is better.

Keep Credit Utilization Low

- Credit utilization ratio means how much credit you are using compared to your total available credit limit. A high ratio shows you are credit-hungry.

- Try to keep your usage below 30% of your total credit limit.

- Example: If your card limit is ₹1,00,000, don’t spend more than ₹30,000 monthly.

Maintain a Healthy Credit Mix

- Having only credit cards or only personal loans can hurt your score. A balanced mix of secured loans (like home or car loans) and unsecured loans (like personal loans or credit cards) improves your profile.

Avoid Applying for Too Many Loans at Once

- Every time you apply for a loan or credit card, bank check your CIBIL report. This is called a hard inquiry, and too many inquiries in a short time negatively affect your score. Apply only when necessary.

Check Your CIBIL Report Regularly

- Errors in your credit report, such as wrong loan accounts or incorrect payment status, can harm your score. Make it a habit to:

- Download your CIBIL report at least once a year.

- Report any mistakes immediately to CIBIL for correction.

Don’t Close Old Credit Accounts

- The length of your credit history matters. If you close an old credit card or loan account, your overall credit history may shrink, lowering your score. Keep old accounts active, especially those with a clean repayment record.

Increase Your Credit Limit, But Use Wisely

- If your bank offers to increase your credit card limit, accept it. A higher limit reduces your credit utilization ratio, which can help improve your score. But remember, don’t overspend just because you have more credit available.

Convert Big Purchases into EMIs

- If you make large purchases on a credit card, convert them into EMIs rather than paying late. This ensures you repay in manageable installments without missing deadlines.

Avoid Being a Loan Guarantor Carelessly

- When you become a guarantor for someone else’s loan, their repayment behavior also impacts your CIBIL score. If they default, your score can suffer too. Always be cautious before agreeing.

How Long Does It Take to Improve CIBIL Score?

Improving your CIBIL score is not an overnight process. With consistent efforts like timely repayments, low credit utilization, and responsible borrowing, you can see improvement in 6–12 months. Severe cases of defaults may take longer.

Benefits of a High CIBIL Score

- Easier approval for personal loans, home loans, and car loans.

- Access to premium credit cards with high rewards.

- Negotiation power for lower interest rates.

- Higher chances of getting pre-approved loans.

Also Read:- Postmen to Be Trained as Mutual Fund Distributors in Small Towns

Final Thoughts

Your CIBIL score is like a report card. A low score can make it hard to get credit, while a high score opens the door to better financial opportunities. By paying bills on time, using credit wisely, and monitoring your credit report, you can steadily increase your CIBIL score and build a strong financial foundation.

Remember, improving your score requires patience and discipline, but the long-term benefits are worth the effort.