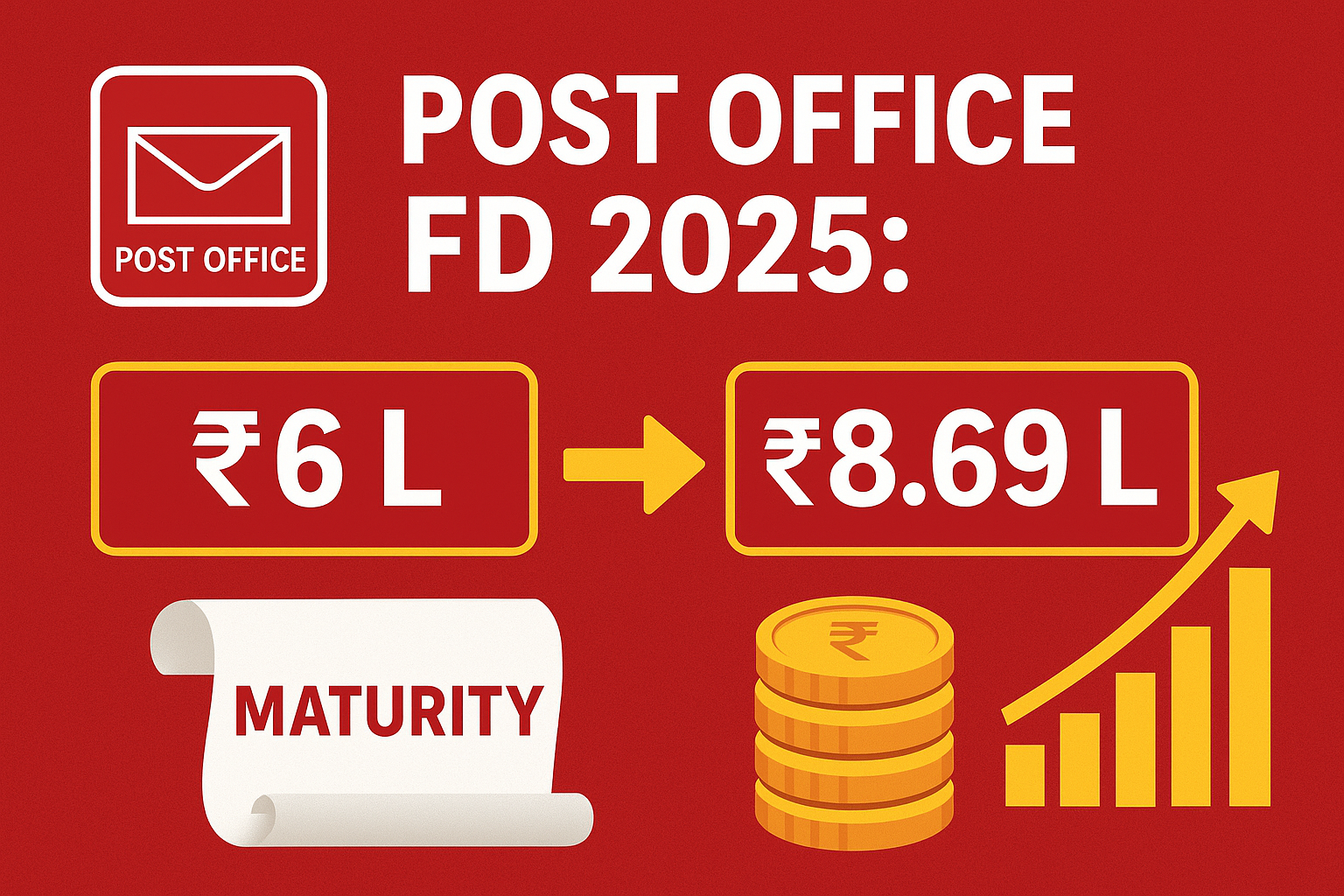

Post Office FD Scheme: ₹6 Lakh Investment Grows into ₹8,69,969 – Here’s How

When it comes to safe and reliable investment options in India, the Post Office Fixed Deposit (FD) Scheme remains one of the most trusted choices. Known for its guaranteed returns and government backing, this scheme continues to be a preferred savings plan for middle-class families, retirees, and conservative investors.

Let’s explore how a ₹6 lakh FD investment in a Post Office can grow into a substantial amount of ₹8,69,969 over a 5-year and why this remains a smart financial move in this year.

Why Choose Post Office Fixed Deposit?

The Post Office FD scheme is ideal for individuals who prioritize security over high risk. Not everyone is comfortable with volatile investments like stocks For such investors Post Office FDs offer:

- Guaranteed returns

- Fixed interest rate throughout the tenure

- Government assurance

- Flexible options ranging from 1 to 5 years

In 2025, the interest rate on a 5-year Post Office FD is approximately 7.5% per annum, which is highly competitive for a low-risk investment product. What makes it even better is the quarterly compounding of interest, which significantly boosts the maturity amount.

₹6 Lakh FD Grows into ₹8,69,969 – The Power of Compounding

Let’s understand the math behind this growth.

- If you invest ₹6,00,000 in a Post Office FD at 7.5% interest per annum compounded quarterly for 5 years, your investment will grow as follows:

- Deposit Amount Interest Rate Tenure Maturity Amount Total Interest Earned

₹6,00,000 7.5% p.a. 5 Years ₹8,69,969 ₹2,69,969 - That’s a gain of nearly ₹2.7 lakh over 5 years—without taking any market risk.

How It Works:

The interest earned every quarter gets added to the principal, and the next quarter’s interest is calculated on the increased amount. This is called compound interest, and it plays a powerful role in growing your money steadily over time.

- Practical Uses of the Maturity Amount

- After five years, the maturity amount of ₹8.69 lakh can be used in multiple ways:

- Higher education for your children

- Down payment for a home or vehicle

- Seed capital for starting a small business

- Emergency fund for medical needs

- Wedding expenses or home renovation

- What’s important is that your money remains safe and earns more than a regular savings account.

- Emotional Value of Secure Saving

For many Indian families, saving money is not just a financial act—it’s an emotional commitment to a secure future. While investing in market-linked instruments can be unpredictable, Post Office FDs offer peace of mind.

Think of it as planting a seed. You nurture it patiently, and after a few years, it grows into something valuable. Investing ₹6 lakh today may feel like parting with liquidity, but in the long run, it becomes a safety net for your family.

Key Benefits of Post Office FD in 2025

- Risk-Free Investment: No exposure to market volatility

- Fixed Returns: Know your maturity amount in advance

- Compounding Advantage: Quarterly compounding increases returns

- Tax Benefits: 5-year FDs qualify for Section 80C deductions (up to ₹1.5 lakh)

- Wide Accessibility: Available at all India Post branches

Final Thoughts

Investing in a Post Office FD of ₹6 lakh for 5 years at 7.5% annual interest can grow into ₹8,69,969 by the end of the term. It’s a smart, secure, and government-backed option for anyone who values capital protection and predictable returns.

In a time where financial uncertainty is common, the Post Office FD Scheme remains a reliable pillar of savings—especially for middle-class households seeking steady financial growth without the need for AI-driven decisions.

Also Read : Canara Bank Home Loan Procedure for 2025: Updated Steps Information

Disclaimer:

This article is intended for educational purposes only. The interest rates and figures mentioned are based on current data available as of August 2025. Rates are subject to periodic revision by the government. Please confirm the latest details with your nearest Post Office branch or official India Post website before investing.